》View SMM Cobalt and Lithium Product Prices, Data, and Market Analysis

》Subscribe to View Historical Spot Price Trends of SMM Cobalt and Lithium Products

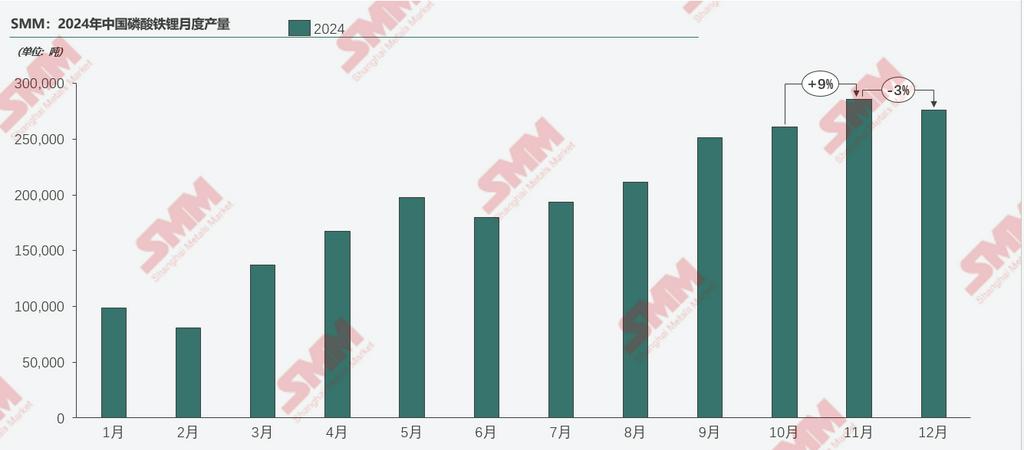

【SMM January 13】According to SMM survey data, China's total production of LFP cathode materials in 2024 exceeded 2.3 million mt, up approximately 84% YoY. The 2024 capacity reached nearly 4.7 million mt, up about 34% YoY, with an annual industry operating rate of approximately 50%, higher than in 2023. The industry's production CR5 was about 56%, and CR10 was around 75%, indicating a slight decrease in concentration compared to 2023.

In 2024, China's LFP material production showed a steady upward trend. At the beginning of the year, the operating rate was low due to the Chinese New Year, but starting from Q2, the industry experienced rapid growth in key regions: first, the post-holiday trade-in policy stimulated demand, leading to increased orders and higher production. There was a slight correction mid-year. Then, the September-October peak season, traditionally a strong demand period for the NEV industry, drove the second wave of production growth. Contrary to expectations of a year-end slowdown, Donald Trump's re-election as US President introduced policy uncertainties, prompting downstream battery manufacturers to rush for installations and exports, reversing demand trends and increasing orders for material manufacturers.

2024 Price Review:

In 2024, the price of LFP cathode materials in China was significantly influenced by the price fluctuations of key raw materials such as lithium carbonate and iron phosphate, as well as the overall market supply and demand structure. However, lithium carbonate, as the primary cost component of LFP, played a decisive role in the price trend of LFP. In 2024, lithium carbonate prices continued to decline, with an annual drop of about 25%, leading to a corresponding decrease in LFP prices. Due to sufficient LFP capacity and intense market competition, battery cell manufacturers used bidding processes to suppress LFP processing fees, leaving most LFP cathode enterprises with weak bargaining power against leading battery cell manufacturers, facing losses and overall continued deficits. LFP processing fees failed to rise significantly, and the overall price trend remained downward.

In price negotiations, cathode manufacturers and battery cell manufacturers primarily discussed LFP processing fees. Leading battery cell enterprises typically conducted semi-annual and annual negotiations, maintaining strict cost control. However, new LFP enterprises competed for market share with low prices, often winning bids with processing fees below market expectations, breaking the price floor. Leading LFP enterprises, with large capacity and advantages in products, costs, and technology, as well as stable financial and supply chains, were relatively better positioned.

Quarterly Analysis:

In Q1, overall LFP prices were relatively stable, mainly due to weak supply and demand during the Chinese New Year holiday, with reduced inventory. By late February, the end-user new energy market recovered, downstream LFP procurement increased, and the market gradually warmed up, with supply and demand both rising, maintaining overall stability. In mid-to-late February, the market recovery was evident, but manufacturers had limited bargaining space, with prices operating near cost levels.

In Q2, the market continued to recover at the beginning of the quarter. Industrial-grade monoammonium phosphate prices rose sharply, coupled with a slow upward trend in lithium carbonate prices, indicating a potential price increase. By the end of Q2, prices began to decline as lithium carbonate prices fell.

In Q3, the market entered the NEV peak season, with strong demand and increased production. However, as raw material prices for iron phosphate and lithium carbonate both declined, LFP prices continued their downward trend. Due to the relatively low technical barriers for mid-end power products and sufficient supply, bargaining power was weak, accelerating the price decline.

In Q4, year-end demand surged due to overseas rush for installations and other factors, pushing the industry's operating rate above 60%. However, raw material prices remained relatively stable, and LFP prices were relatively stable as well.

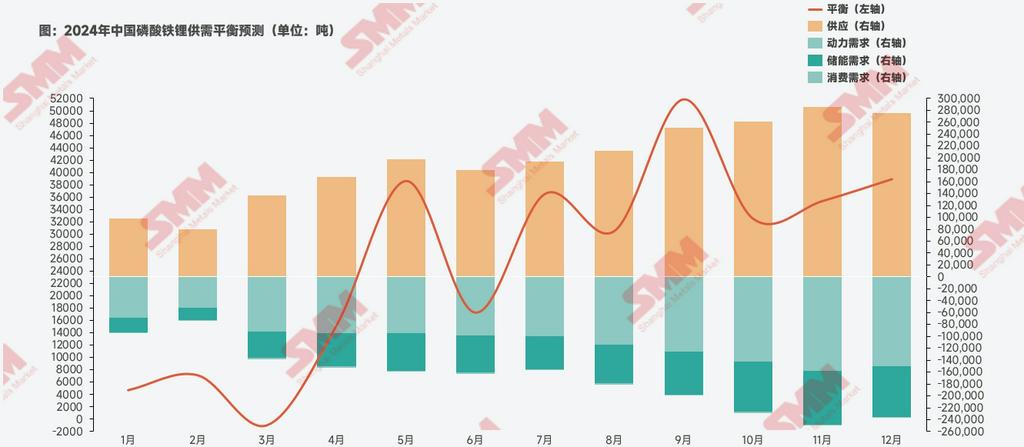

In 2024, the LFP market experienced significant supply and demand fluctuations. Overall, the industry transitioned from destocking in Q1 to inventory buildup. From Q2 onward, the supply-demand gap gradually widened. Although mid-year production slightly declined, causing demand to slightly exceed supply, the gap quickly widened again, resulting in a surplus for the year.

Exports and Overseas: In 2024, China's total LFP exports were approximately 2,600 mt, representing a YoY growth of over 120%. The top five export destinations were South Korea, Vietnam, Taiwan, China, Norway, and France. Regarding overseas capacity, overseas LFP capacity in 2024 was about 30,000 mt. With more Chinese LFP enterprises accelerating their overseas expansion, capacity is expected to increase in 2025.

2025 Price Outlook

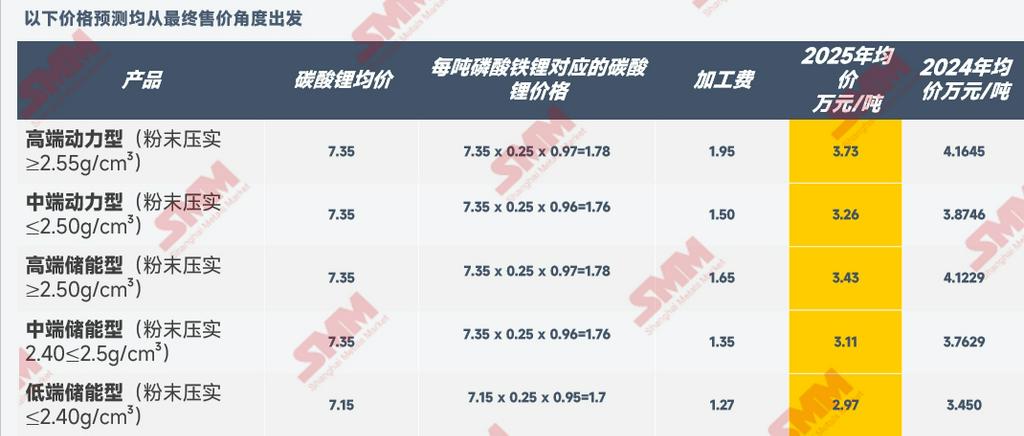

In 2025, the market is expected to continue facing the challenge of overcapacity. New capacity expansions are anticipated in 2025, and although demand is expected to gradually rise, the overall growth rate will likely lag behind capacity and production. Combined with further declines in lithium carbonate prices due to increased surplus levels in 2025, the downward price trend for LFP materials is unlikely to reverse. However, given the current limited production of high-density powder materials (with compaction density exceeding 2.55 g/cc), which are scarce and not widely available for mass production and delivery, these materials are expected to have stronger bargaining power, potentially driving up processing fees and achieving profitability. For products with a compaction density of 2.45 g/cc or below, the losses are unlikely to improve. Below is the 2025 LFP material price forecast for reference:

SMM New Energy Research Team

Cong Wang 021-51666838

Xiaodan Yu 021-20707870

Rui Ma 021-51595780

Ying Xu 021-51666707

Disheng Feng 021-51666714

Yujun Liu 021-20707895

Yanlin Lü 021-20707875

Ye Yuan 021-51595792

Zhicheng Zhou 021-51666711

Haohan Zhang 021-51666752

Zihan Wang 021-51666914

Xiaoxuan Ren 021-20707866

Yushuo Liang 021-20707892

Jie Wang 021-51595902

Yang Xu 021-51666760

Boling Chen 021-51666836